4.52.090 Exemption – Duration – Affordability requirements – Limits.

A. The value of new multifamily housing construction improvements qualifying under this chapter shall be exempt from ad valorem property taxation for 12 successive years, beginning January 1st of the year immediately following the calendar year of issuance of the final certificate, and provided the following affordability requirements are satisfied:

1. Except as provided in subsections (A)(2) and (A)(3) of this section, a minimum of 20 percent of the project’s total units must be affordable units with affordable rents as follows:

a. Any dwelling unit that is 320 square feet or less shall be categorized as a very small dwelling unit. Any affordable unit that is a very small dwelling unit shall have an affordable rent at or below 50 percent of the King County median income, adjusted for household size.

b. Any affordable unit that is not a very small dwelling unit shall have affordable rents at or below 80 percent of the King County median income, adjusted for household size.

Unless otherwise stated, nothing in this section shall relieve the owner of complying with the eligibility requirements in BCC 4.52.040.

2. If a project is unable to meet the MFTE program’s eligibility requirement that a minimum of 15 percent of its total units have two or more bedrooms, then the project may still qualify for the MFTE program provided it selects one of the following:

a. A minimum of 25 percent of the project’s total units are affordable units and shall have affordable rents at or below 80 percent of the King County median income, adjusted for household size; or

b. A minimum of 20 percent of the project’s total units are affordable units and shall have affordable rents at or below 70 percent of the King County median income, adjusted for household size; except any affordable units having two or more bedrooms shall remain at or below 80 percent of the King County median income, adjusted for household size.

Nothing in this section shall relieve the owner of the affordability requirements for very small dwelling units under subsection (A)(1) of this section.

3. An eligible project may benefit from both the MFTE program and other incentive programs that seek to increase the quantity of affordable housing. When a project utilizes both the MFTE program and another incentive program, the project shall apply the MFTE benefit as follows:

a. Overlap. When a project overlaps the MFTE benefit with units that also receive incentives from another affordable housing program, and said units are used simultaneously to satisfy the requirements of both programs, the affordable rents for said units shall be at least 15 percentage points below the applicable King County median income level, adjusted for household size, as prescribed in this chapter, provided this 15 percent reduction shall not apply to very small dwelling units described in subsection (A)(1) of this section. Thus, by example, when a project overlaps an MFTE unit as described in subsection (A)(2)(b) of this section with another affordable housing program, said unit would have affordable rents at or below 65 percent of the King County median income, adjusted for household size; or

b. No Overlap. When a project does not overlap the MFTE benefit with units that also receive incentives from another affordable housing program, the affordable units required under this chapter shall be in addition to those that the project is required to designate under the other incentive programs.

c. Illustration.

|

Overlap |

No Overlap |

|---|---|

|

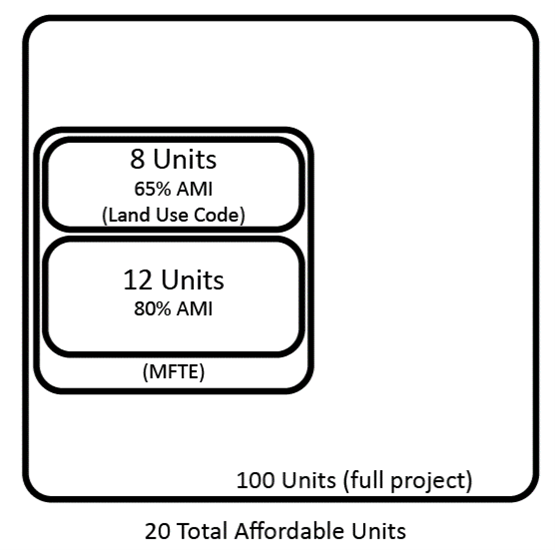

In a 100-unit project, where 8 affordable units are required under an incentive program other than the MFTE program, and 20 affordable units are required under the MFTE program, overlapping the 2 incentive programs for a total of 20 affordable units, then for 12 years the affordable rents for the 8 overlapping units shall be at or below 65 percent of the King County median income, adjusted for household size, and the affordable rents for the remaining 12 units shall be at or below 80 percent of the King County median income, adjusted for household size. When the exemption expires or terminates, the project must continue to provide the 8 affordable units as required under the other incentive program.

Note: Illustration assumes the project satisfies the 15 percent requirement under BCC 4.52.040(F) and does not include very small dwelling units. |

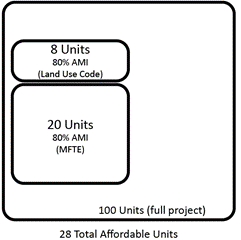

In a 100-unit project, where 8 affordable units are required under an incentive program other than the MFTE program, and 20 affordable units are required to be set aside under the MFTE program, for a total of 28 affordable units, then the affordable rents for the 20 MFTE units shall be at or below 80 percent of the King County median income for the duration of the MFTE program. The project must provide the 8 additional affordable units consistent with the other incentive program’s requirements.

Note: Illustration assumes the project satisfies the 15 percent requirement under BCC 4.52.040(F) and does not include very small dwelling units. |

Nothing in this chapter shall relieve a project of observing more restrictive criteria prescribed under another affordable housing incentive program.

4. For any affordable units required in this section, the following shall apply:

a. Affordable units shall have affordable rents as defined in BCC 4.52.020(B).

b. The mix of unit types (e.g., very small dwelling unit, studio, one-bedroom, two-bedroom, etc.), configuration and size of affordable units at each affordability level shall be substantially proportional to the mix, configuration and size of the total housing units in the project unless otherwise approved by the director.

c. Affordable units will be reserved for occupancy by eligible households who certify that their household income does not exceed the applicable percentage of the King County median income; and who certify that they meet all qualifications for eligibility, including any requirements for recertification on income eligibility as set forth in the MFTE covenant referenced in BCC 4.52.040(E).

d. When the project contains more than one building or multiple floors, all of the affordable units required by this chapter may not be located in the same building or on the same floor. The affordable units shall be interspersed with all other dwelling units within the project.

e. If, in calculating the number of affordable units, the number contains a fraction, then the number of affordable units shall be rounded up to the next whole number.

B. The exemption does not apply to the value of land or to the value of improvements not qualifying under this chapter, to increases in assessed valuation of land and nonqualifying improvements, or to increases made by lawful order of the King County board of equalization, Washington State Department of Revenue, State Board of Tax Appeals, or King County, to a class of property throughout the county or a specific area of the county to achieve uniformity of assessment or appraisal as required by law. (Ord. 6765 § 1, 2023; Ord. 6582 § 13, 2021; Ord. 6400 § 2, 2018; Ord. 6231 § 2, 2015.)